Average Settlement for a Non-Injury Car Accident: What to Expect

When you’re involved in a non-injury car accident, the settlement usually focuses on property damage instead of medical bills or pain and suffering. The average settlement for a no-injury car accident may include vehicle repair costs, total loss value, towing fees, rental car expenses, and possible diminished value.

In this guide, you’ll learn what affects a property damage-only car accident settlement, how insurance companies calculate payouts, and what steps can help you negotiate a fair offer.

Key Takeaways

Non-injury car accident settlements usually focus on vehicle and property damage.

Common payouts may include repairs, total loss value, towing, and rental car costs.

Emotional distress or inconvenience compensation is usually limited in no-injury claims.

Your settlement depends on damage severity, vehicle value, fault, and insurance limits.

Do not accept the first insurance offer without reviewing repair estimates and evidence.

Understanding Non-Injury Car Accidents

What Counts as a Non-Injury Car Accident?

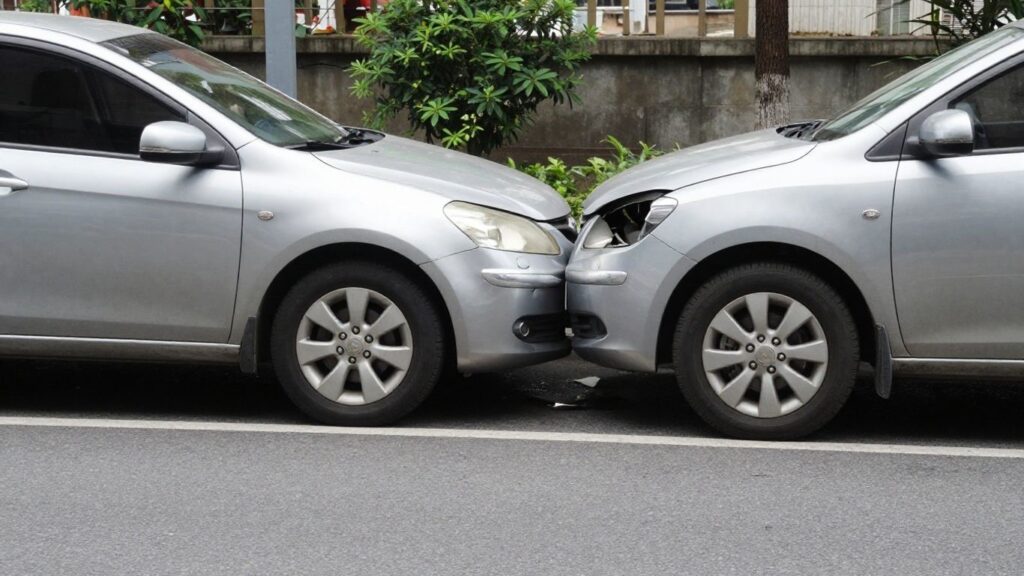

A non-injury car accident is a property-damage-only crash where no driver, passenger, pedestrian, or cyclist reports physical injuries. These claims usually focus on repairing or replacing the damaged vehicle, paying towing or rental costs, and resolving any property damage caused by the accident.

Also called a property-damage-only accidentYou’ve just been in an auto accident, but fortunately, no one was injured. So that is the most important, isn’t it? A non-injury car accident, also referred to as a property-damage-only (PDO) accident, is just what it implies: a car accident in which the damage is done to the vehicles and other property, but not to individuals.

That is, no broken bones, no whiplash, no trips to the emergency room. No longer is it just about the damage to your car, truck, or bike, but about damage to anything else that may have been touched, such as fences or guardrails.

In these cases, the primary objective is to get your car fixed or replaced and to provide you with compensation for the inconvenience and loss of use of your car. It may appear easier than a case with injuries; however, there are actions you can take to ensure that you receive reasonable compensation. Essentially, you are dealing with property damage claims and, at times, the hassle factor.

The anxiety associated with an accident can be a big stress without having sustained any personal injuries. The hassle of dealing with insurance companies, obtaining repair quotations, and making it easy to get a rental car can be quite annoying. Remember, you have time and peace of mind as well.

If you want a broader overview of what steps to take after any accident, check this guide: what to do after a car accident

Common Scenarios of Non-Injury Accidents

Non-injury car crashes happen all the time, and they come in many forms. You might have been involved in:

Rear-End Collisions

Minor rear-end crashes may damage bumpers, sensors, lights, trunks, or rear panels even when no one is injured.

Parking Lot Fender Benders

Low-speed parking accidents often involve dents, scratches, side mirror damage, or bumper repairs.

Intersection Collisions

Even low-speed intersection crashes can cause costly damage to bumpers, wheels, sensors, and body panels.

Single-Vehicle Accidents

These may involve hitting a pole, wall, fence, mailbox, guardrail, tree, or another fixed object.

Hit-and-Run Property Damage

If the other driver leaves, your own collision or uninsured motorist property damage coverage may matter.

Minor Multi-Car Damage

Some low-speed crashes involve several vehicles, making fault and insurance responsibility more complicated.

In all of these cases, determining the value of a car accident injury without any bodily damage may be relatively simple, but it is not always simple. Some of the things you’ll be considering are the Blue Book value of your vehicle and the cost of repairs. The first step to getting back on track after a minor car accident is to understand what to expect.

Keep in mind, even if the accident is a minor one, it can make a big difference in your life, and it’s important to understand how much compensation is available in the event of a non-injury car accident.

Even minor crashes can impact your finances. Understanding settlement expectations is important, especially when comparing with typical payouts discussed here: average personal injury settlement amounts

Why Settlements Differ in Non-Injury Cases

You’ve had a car accident, but fortunately, nobody was injured. That’s the most crucial thing, isn’t it? But with the car now damaged, you’re wondering about how much to expect for a fender bender settlement. Not quite as simple as it sounds, and your earnings will differ greatly. The final number is affected by a few factors.

Factors Influencing Settlement Amounts

The insurance companies consider a couple of factors when determining a non-injury car accident settlement. First off, they’ll check the value of your car before the accident happened. It’s more than just what you paid for it; it’s about what it’s worth today based on its age, mileage, and condition. Then there’s the cost of repairs. If your car is repairable, they’ll provide an estimate of the cost of the repairs. If they consider the damage too extensive, they may decide to consider it a total loss and give you the actual cash value instead.

Here’s a quick look at what plays a role:

Vehicle Value

The car’s age, mileage, condition, trim, and market value affect the settlement amount.

Repair Cost

Body work, sensors, paint, frame damage, and labor rates can increase the claim value.

Fault

If you are partly responsible, the payout may be reduced depending on state law and policy terms.

Policy Limits

The at-fault driver’s property damage limit may cap how much their insurer can pay.

If you’re comparing accident payouts, this detailed guide helps: how much is a car accident settlement worth

The Role of Property Damage

The primary incident in a non-injury accident is property damage. This includes the cost to fix your vehicle or the value of your car, if your vehicle is totaled, before the crash. You may also receive reimbursement for such costs as towing, rental car costs while you are having your vehicle towed, and even a reduction in the value of your vehicle after it is fixed (known as diminished value).

It’s important to have solid documentation for all of this. Obtain a repair quote from a good repair shop. When a car is a total loss, the insurance company will provide you with its valuation.

If you like, you can look up the value of your car with a site such as Kelley Blue Book or NADA Guides to determine if the quote is reasonable. If you don’t agree with their evaluation, you can appeal. It’s even possible to have a third-party appraisal to support your claim. Here, the insurance company’s value is important.

What a Non-Injury Car Accident Settlement May Cover

Most property-damage-only settlements focus on repairing, replacing, or reimbursing costs related to the damaged vehicle.

| Settlement Item | What It Means | Why It Matters |

|---|---|---|

| Vehicle Repairs | Payment for body work, paint, parts, sensors, lights, and mechanical damage. | This is usually the largest part of a no-injury accident settlement. |

| Total Loss Value | If repairs cost more than the car is worth, the insurer may pay actual cash value. | You should compare the insurer’s valuation with market data. |

| Towing Costs | Reimbursement for towing from the crash scene or storage facility. | Keep receipts because insurers usually require documentation. |

| Rental Car | Temporary transportation while your vehicle is being repaired or valued. | This may depend on fault, policy coverage, and repair timeline. |

| Diminished Value | Possible loss in resale value after the car has been repaired. | This is more common with newer or higher-value vehicles. |

Proper documentation is key. If disputes arise, understanding timelines can help: how long a personal injury case takes

Assessing the Value of Your Claim

If you’re trying to navigate what to anticipate after a fender bender settlement, bear in mind that it is all about the property damage! Injury is not the issue here: no medical expenses or lost wages to think about. You can still get compensation for the hassle and stress the accident has caused you, however. These are typically smaller than what you would get in an injury case, and can be the loss of use of your vehicle or emotional distress.

The first settlement from an insurance company is typically only a settlement. They are businesses, and their objective is to deal with claims in the least expensive way. If you think it is not enough to compensate you, don’t hesitate to negotiate. You will be able to prove a fair amount of property damage settlement amount in a car accident in a better manner if you have a clear understanding of your car’s worth, as well as have documents to prove it. Keep in mind that the purpose of the exercise is to have your vehicle repaired and returned to its condition before the accident, or to have a fair settlement.

While a settlement for a fender bender may seem like an annoying process, it tends to be faster than injury claims since you don’t have to wait for your body to heal. For most property damage only claims, a few weeks to a couple of months is enough time until the repair is finished, unless there is a big dispute over the amount of the repair or the worth of the vehicle.

However, emotional distress claims are usually limited compared to serious cases (explained here: how much can I sue my landlord for emotional distress).

The Claims Process for Non-Injury Accidents

Thus, you have been involved in an accident, but fortunately, nobody was injured. The most important thing is that, right? You might be thinking, “What do I do now?” particularly when it involves having to get your vehicle repaired or replaced.

The claims process for a non-injury car accident is typically simpler and more streamlined compared to an injury accident, but it is still crucial to pay attention to the details. The aim is to have your car repaired back to pre-accident condition or fairly paid for its worth.

Gathering Evidence and Documentation

This is where you lay the groundwork for your entire claim. Without solid proof, insurance companies might try to offer less than what your vehicle is actually worth. Think of it as building your case.

Evidence Checklist for a Non-Injury Accident Claim

Strong documentation can help you prove the value of your property damage claim.

- Photos and videos: Capture vehicle damage, scene position, license plates, road signs, and nearby property damage.

- Driver information: Save the other driver’s name, contact details, insurance information, and license plate number.

- Police report: Get the report number if law enforcement responds to the crash.

- Repair estimates: Collect at least two or three estimates from reputable repair shops.

- Receipts: Keep towing, storage, rental car, rideshare, and other accident-related expense records.

These steps are similar to other incidents like what to do after a motorcycle accident or bicycle accidents.

Filing an Insurance Claim

If you have all your ducks in a row, it’s now time to reach out to the insurance companies. Typically, the claims process will be with the Insurance Company of the wrong driver. But there is also the option of having your own insurance carrier to whom you can submit a claim, particularly if you have collision coverage. They may cover the costs of your repairs, but then try to recover from the other party’s insurance company.

Here’s a general idea of what to expect:

- Report the Accident: Contact the insurance company (or companies) involved. You’ll need to provide details about the accident.

- Adjuster Assignment: An insurance adjuster will be assigned to your case. They’ll review the information you provide and may want to inspect the vehicle themselves.

- Damage Assessment: The adjuster will assess the damage to your vehicle and determine the cost of repairs. They’ll also decide if the vehicle is a total loss (meaning the repair cost exceeds its market value).

- Settlement Offer: Based on their assessment, the insurance company will make a settlement offer. This is often where negotiation comes in, especially if you feel the offer doesn’t fully cover your losses. Remember, the initial offer is rarely the final one.

Be aware that insurance companies often aim to settle claims quickly and for the least amount possible. It’s important to be patient and thorough, and not to feel pressured into accepting an offer that doesn’t seem fair. The average payout for a fender bender can vary wildly, so don’t rely solely on what others received.

If your situation becomes complex (like multi-vehicle accidents), you may also find guidance here: what to do after a truck accident

Negotiating a Settlement

This is a critical step in getting the compensation you deserve for your car accident property damage payout. Don’t just accept the first offer you receive. Insurance adjusters are trained negotiators, and they often start with a lower figure.

Do Not Accept the First Offer Too Quickly

The first insurance offer may not fully reflect your repair costs, rental car expenses, towing fees, or diminished value. Review the offer carefully and compare it with your own documentation before agreeing to settle.

- Compare the insurer’s estimate with independent repair quotes.

- Ask whether OEM parts, labor rates, rental costs, and taxes are included.

- Request a written explanation if the offer is lower than your documentation supports.

- Use repair invoices, market value data, and photos to support your counteroffer.

Remember, the process for a car accident property damage claim value is focused on restoring your property. While it might not involve the complexities of injury claims, it still requires diligence to ensure you’re not shortchanged.

If negotiations get difficult, understanding how much a personal injury lawyer costs can help you decide whether to bring in legal support.

When to Seek Legal Advice

The vast majority of the time, a car accident with no injuries is fairly simple. You collect your repair quotes, possibly a rental car charge, and a check comes from the insurance company. Easy peasy, right? However, certain instances are slightly messy, and that’s when you may wish to look at engaging a specialist.

Don’t hesitate to get a lawyer involved if the other driver is disputing fault or if the insurance company is being difficult. It’s not uncommon for adjusters to try to lowball you, especially if they think you don’t know what you’re doing. They know how to deal with this type of situation, and you likely don’t.

Here are a few situations where having an attorney in your corner can make a big difference:

Fault Is Disputed

If the other driver denies responsibility, legal guidance can help protect your claim.

Repair Offer Is Too Low

If the insurer’s repair estimate does not match shop estimates, you may need support.

Total Loss Value Is Unfair

If the insurer undervalues your vehicle, an appraisal or legal review may help.

Insurance Delays or Denials

If the insurance company delays, denies, or acts unfairly, speak with a professional.

After an accident, the insurance company can be a pain to deal with. They have people on staff whose job it is to pay out as little as possible. If you feel that you are not being treated fairly or if there is more to it than you first thought, perhaps it is time to speak with a lawyer. Many will meet with you on a free basis to answer questions about the process, so you have nothing to lose by asking any questions that you may have.

Keep in mind, many cases do not require legal assistance, and if it does, it is important to know when to call in a backup to save yourself time, stress, and maybe a lot more money. It’s always better to be prepared and understand your options, especially when it comes to getting fair compensation for your vehicle damage.

In such cases, consulting a professional like a truck accident lawyer or slip and fall lawyer can guide you, even if your case is smaller.

Focus on Proof, Not Guesswork

A fair non-injury car accident settlement depends on clear evidence of your property damage, vehicle value, repair costs, towing fees, rental expenses, and any diminished value. The stronger your documentation is, the easier it becomes to challenge a low insurance offer and negotiate a reasonable payout.

Conclusion

Even if nobody is injured, a car accident can still cause a headache, primarily because of car repairs and transportation without your car. Settlements for these types of accidents are typically not as high as settlements for injuries, but they are still significant. It’s all about repairing or replacing your car and paying for or dealing with any expenses or hassles resulting from the accident.

It’s important to keep in mind that the insurance company may not be providing the best amount right away, so take the time to discuss it with them and don’t hesitate to request what you deserve. The primary concern here is to get back on the road.

Frequently Asked Questions

Here are quick answers about non-injury car accident settlements, property damage claims, insurance payouts, repair costs, and when legal help may be needed.

What is the average settlement for a non-injury car accident? +

The average settlement for a non-injury car accident usually depends on the vehicle damage, repair cost, total loss value, towing fees, rental car expenses, and who was at fault. Since there are no medical bills or injury damages, the settlement is usually based mainly on property damage.

What does a non-injury car accident settlement usually cover? +

A non-injury car accident settlement may cover vehicle repairs, replacement value if the car is totaled, towing costs, storage fees, rental car costs, and sometimes diminished value. It usually does not include medical bills because no physical injury is involved.

Can I get compensation for inconvenience after a no-injury accident? +

Compensation for inconvenience is usually limited in a no-injury accident claim. However, you may be able to recover related out-of-pocket costs such as rental car expenses, towing fees, rideshare costs, and loss of use while your vehicle is being repaired.

What happens if my car is totaled but no one was injured? +

If your car is totaled in a non-injury accident, the insurance company may offer the actual cash value of the vehicle before the crash. You should review the valuation carefully and compare it with local market prices, mileage, condition, trim level, and similar vehicles for sale.

Should I accept the first insurance offer? +

You should not accept the first insurance offer without reviewing it carefully. Compare the offer with repair estimates, towing receipts, rental costs, vehicle value reports, and any diminished value evidence. If the offer is too low, you can negotiate with supporting documents.

How long does a non-injury car accident claim take? +

A simple non-injury car accident claim may settle within a few weeks, especially if fault is clear and repair costs are not disputed. It can take longer if the insurance company disagrees about fault, repair costs, total loss value, or diminished value.

Do I need a lawyer for a non-injury car accident? +

You may not need a lawyer for a simple property-damage-only accident. However, legal advice may help if fault is disputed, the insurer delays your claim, your vehicle is undervalued, repair estimates are unfairly low, or the insurance company refuses to pay valid expenses.

Can I claim diminished value after a non-injury accident? +

You may be able to claim diminished value if your repaired vehicle is worth less because it now has an accident history. This is more common with newer vehicles, higher-value vehicles, or cars with significant damage. You may need an appraisal or market evidence to support the claim.